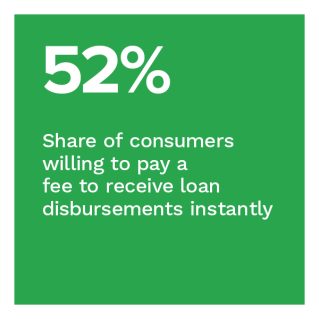

Consumers in the United States frequently receive disbursement payments, whether it be Social Security payments, tax refunds, insurance claim payouts or bonus payouts. In the last year, 63% of consumers received a disbursement — and 68% want the choice to receive their disbursement payment instantly, an increase from the 47% that said the same in our “Disbursement Satisfaction Report 2022.” Some consumers would even be willing to pay a fee for an instant payment — especially those struggling financially.

While demand for these instant payments increases, many payers still do not offer instant options, and growth in instant payments adoption among payers has stagnated. But even when a payer offers the option for an instant payment, other factors cause consumers to choose another method, including a lack of trust in their payment or data security and the fee that may come with receiving an instant payment.

The “Disbursements Satisfaction Report 2023: Instant Payouts Reach an Inflection Point,” a PYMNTS and Ingo Money collaboration, provides a snapshot of the state of the disbursements space in the United States. We surveyed a census-balanced panel of 2,292 U.S. consumers to examine the number and types of disbursements they received in the past year and discover how they received them. This is the sixth year we have done this report, providing insight into consumers’ growing interest in instant disbursements and the factors service providers can address that could change consumer perception of receiving instant payments and maximize consumer satisfaction.

Key findings from this report include the following:

• Consumers choose instant payment options 68% of the time, even though just 22% received an instant disbursement in the past 12 months.

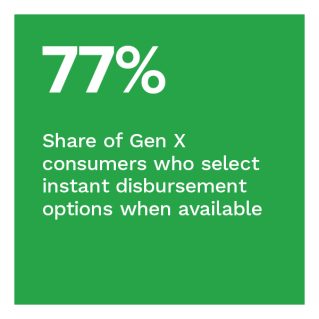

Most consumers prefer to receive their payout as an instant deposit to a bank account, twice as popular as the next preferred payment method. Nearly half of the consumers who payers did not offer an instant payment method say they would like that option. Generation X and middle-income consumers are particularly likely to choose instant payment options when payers offer them.

• Offering financial incentives are effective in shifting consumer payout preference, even toward payout options that are not instant.

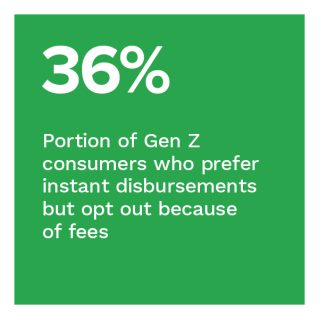

The most common reason why consumers amenable to instant disbursements opted out is that the firms offered a financial incentive to use a different method, at 32% of consumers, followed by 29% who did not choose an instant payment option because they would have to pay a fee to receive the funds instantly.

• Consumers are not interested in receiving instant payouts for several reasons, with security concerns topping the list.

Two of the three most common reasons why consumers choose not to use instant disbursements pertain to fears regarding data and account security. Thirty-six percent of consumers who had the option to use instant disbursements chose another method because they did not want to share their card information, and 33% said they did not utilize an instant disbursement because they did not want to share their bank account information. Moreover, 23% of consumers who prefer instant payments yet used another method did so because they did not trust the service provider to issue an instant disbursement — an indication that data security is just as important for consumers already sold on instant payments as it is for those uninitiated.

To learn more about consumer perception and satisfaction with instant disbursements, download the report.